Day 7 of Australian Rail Series

Your first solo train ride felt like freedom. Today, 400+ million passengers a year take that same journey without a second thought — and the engineering that makes every trip unremarkable is the greatest achievement of a system that barely breaks even.

The Story

When I was twelve, I took a train alone for the first time. I remember the platform — the yellow line, the electronic board flickering, the rush of air as the train arrived. I stepped on board with the studied nonchalance of someone pretending they’d done this a hundred times. The doors closed. The train moved. And suddenly the world was bigger.

That was one journey. One twelve-year-old. One morning.

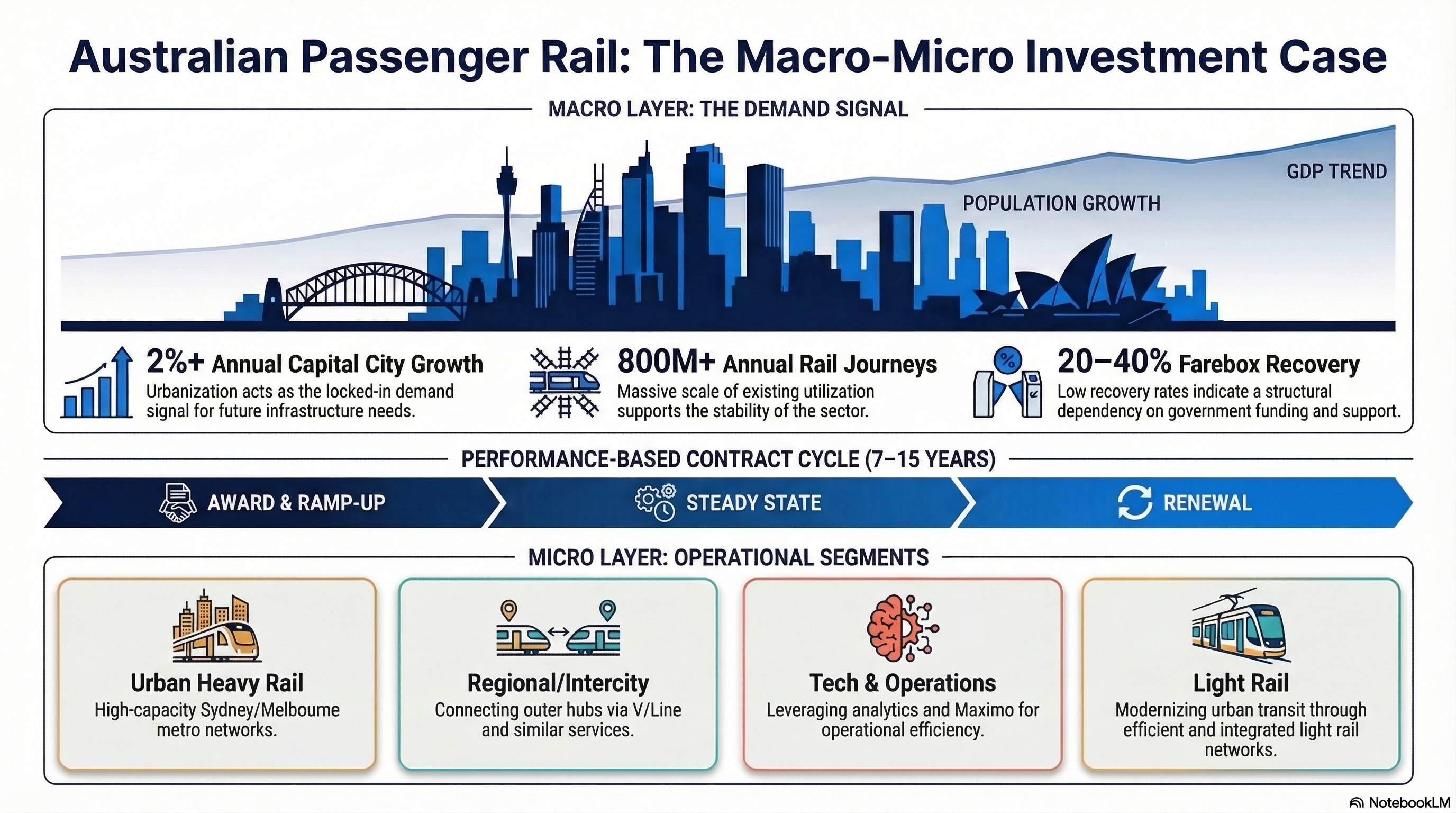

Today, Australian passenger rail carries over 400 million passengers every year. Sydney Trains alone moves more people in a single morning peak than the entire population of Canberra. Melbourne’s tram network is the largest on Earth — bigger than any city in Europe, the continent that invented trams.

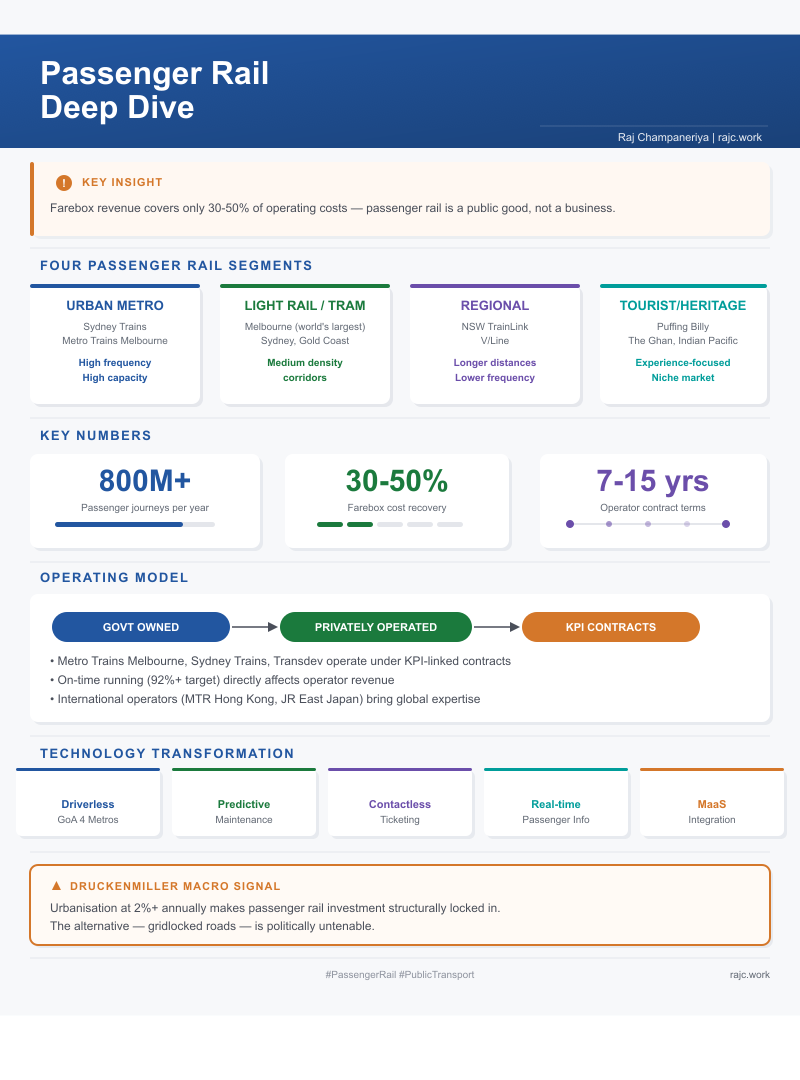

But here’s what hasn’t changed: the paradox. Despite world-class scale, most Australian passenger rail systems are barely profitable. Farebox revenue covers only 30–50% of operating costs. Every journey is subsidised by taxpayers who may never ride a train.

That paradox — a service used by hundreds of millions, funded by everyone, owned by the public, but operated for profit by private companies — reveals everything about how public transport actually works.

Day 7 in pictures

A few visuals for post.

The Deep Dive — 8 Questions

How do four distinct passenger rail segments create fundamentally different maintenance requirements?

Australian passenger rail isn’t one thing. It’s four:

| Segment | Examples | Key Characteristic |

|---|---|---|

| Heavy suburban | Sydney Trains, Metro Melbourne | High-frequency, electrified, double-deck or high-capacity |

| Metro / automated | Sydney Metro | Driverless, platform screen doors, newest technology |

| Light rail / tram | Melbourne trams, Sydney Light Rail | Street-running, mixed traffic, frequent stops |

| Regional / intercity | NSW TrainLink, V/Line | Long-distance, diesel or electrified, lower frequency |

Each segment demands different maintenance: heavy suburban needs intensive track and signalling maintenance (wear from high-frequency services); metro needs specialised automation systems support; trams need embedded track maintenance in operating roadways; regional needs diesel locomotive overhauls and long-line infrastructure upkeep.

A maintenance organisation covering all four segments is operating, effectively, four parallel businesses.

Why does Sydney’s double-deck approach represent a fundamentally different capacity philosophy than Melbourne’s single-deck?

Sydney chose double-deck trains in the 1960s — a bet on maximising seats per train. Melbourne chose single-deck — a bet on faster boarding (more doors, level platforms) and higher service frequency.

Both are valid capacity strategies. Double-deck moves more passengers per train but with longer dwell times at stations (passengers climbing stairs to reach seats). Single-deck moves fewer passengers per train but enables faster turnaround and higher frequency.

The choice, made decades ago, shapes infrastructure today. Sydney’s tunnels and platforms were built for double-deck height. Melbourne’s were built for single-deck clearances. Neither city can easily switch — the decision is baked into concrete.

Why does Melbourne’s tram network — the world’s largest — fill a capacity gap that neither heavy rail nor buses can serve?

Melbourne operates 250 km of tram routes — the largest tram network in the world. It fills a specific capacity niche: too much demand for buses, not enough for heavy rail.

Trams carry 100–200 passengers per vehicle in mixed traffic, serving inner-city corridors where underground rail construction would be prohibitively expensive but bus frequency can’t meet demand. They provide the ubiquity of buses with capacity closer to rail.

The maintenance challenge is unique: embedded track in roadways must be maintained while managing road traffic, power systems include overhead wiring in complex urban environments, and vehicles operate in stop-start conditions that accelerate wear on brakes, bogies, and traction systems.

How do performance-based contracts create accountability tension between profit incentives and public service?

Metro Trains Melbourne operates under a government franchise contract. The state owns the assets. Metro Trains provides operations and maintenance. Payment is tied to performance metrics: on-time running, customer satisfaction, safety.

The model creates accountability — miss KPIs, lose revenue. But it also creates tension. When a disruption occurs, the operator faces a choice: restore the schedule as quickly as possible (protecting OTR metrics and contract payments) or prioritise passenger communication and alternative transport (protecting customer experience but potentially missing the OTR target).

Performance-based contracts work best when the metrics align perfectly with passenger outcomes. They degrade when metrics become targets to be gamed rather than indicators to be improved.

Which technology trend — automation, predictive maintenance, or MaaS — will most transform Australian passenger rail?

Automation is already here: Sydney Metro operates fully driverless (GoA 4), demonstrating that established urban rail services can run without drivers. The impact is transformational — higher frequency, faster recovery from disruptions, lower per-service operating costs.

Predictive maintenance targets the cost base: reducing unplanned failures means fewer service disruptions, lower emergency repair costs, and better asset utilisation. IBM Maximo Health and Predict is designed precisely for this use case.

Mobility-as-a-Service (MaaS) targets the demand side: integrating rail with ride-share, bike-share, and bus in a single platform, solving the first/last mile problem that keeps passengers in their cars.

Each transforms a different dimension. Automation changes operations. Predictive maintenance changes cost. MaaS changes demand. Together, they reshape the entire system.

How has post-COVID patronage recovery reshaped the business case for urban rail investment?

COVID-19 collapsed passenger rail patronage to 10–20% of pre-pandemic levels. By 2026, recovery varies: Sydney has reached approximately 85–90% of pre-COVID patronage; Melbourne is at 80–85%.

The missing 10–20% is mostly peak-hour commuters working from home 1–2 days per week. This structural shift changes the business case: networks designed for five-day peak demand now face three-to-four-day peaks. Revenue falls. Operating costs remain largely fixed.

The policy response is evolving: off-peak fare incentives, leisure travel marketing, and repurposing spare peak capacity for freight. The operators that adapt their service patterns and cost structures to this new demand profile will outperform those waiting for a pre-COVID “normal” that isn’t returning.

Why do international operators like MTR and JR East bring value to Australian passenger rail contracts?

When Australian states tender passenger rail franchises, international operators bring something domestic companies can’t: experience running complex rail networks in other countries.

MTR Corporation (Hong Kong) operates Melbourne’s metropolitan rail franchise. Its experience running one of the world’s most efficient metro systems — 99.9% reliability — provides benchmarks, management systems, and operational culture that lift local performance. JR East (Japan) has been involved in advisory roles for Australian rail projects, sharing Shinkansen maintenance practices and operational discipline.

The value isn’t just technical transfer. International operators bring different safety cultures, different approaches to workforce management, and different expectations about what “world-class” looks like — raising the bar for the entire Australian industry.

Where does IBM’s AI and analytics expertise create the highest-value opportunities in passenger rail?

Three areas where technology investment delivers outsized returns:

- Asset management (Maximo): Rolling stock maintenance for fleets of 500+ carriages, where extending asset life by even 5% saves tens of millions

- Demand forecasting (watsonx): Predicting passenger demand by route, time, and day — enabling dynamic timetabling that matches capacity to actual need

- Cybersecurity (QRadar): Protecting increasingly connected rail operations — from CCTV networks to passenger Wi-Fi to signalling systems — against threats that grow as connectivity increases

The connecting thread: data. Every train generates telemetry. Every fare gate records a transaction. Every signal reports its state. The organisations that turn this data into decisions will outperform those that collect it and file it away.

Synthesis

Australian passenger rail is a diverse ecosystem spanning driverless metros, century-old tram networks, and regional services connecting communities with no alternative transport. The operating model is fundamentally different from freight: passenger services are government-subsidised because farebox revenue covers only 30–50% of operating costs.

The technology transformation underway — automation, predictive maintenance, contactless ticketing, MaaS — is reshaping both operations and the competitive landscape. But the ultimate measure of success hasn’t changed since my first solo train ride: did the passenger get where they were going, safely, on time, without having to think about how it happened?

Vocabulary Spotlight

| Term | Definition |

|---|---|

| Farebox recovery ratio | The proportion of operating costs covered by passenger fare revenue; Australian urban systems typically recover 20–40% |

| Performance-based contract | An operator agreement where payment is tied to meeting defined service levels (OTR, safety, cleanliness) |

| Dwell time | The duration a train stops at a station for boarding and alighting; a key driver of journey time and network capacity |

Macro Signal

Druckenmiller Macro: The macro force driving passenger rail investment is urbanisation. Australia’s capital cities are growing at 2%+ annually, and public transport capacity is the binding constraint on urban density. Every new apartment tower increases demand for rail capacity. Passenger rail investment is structurally locked in regardless of political cycle because the alternative — gridlocked roads and voter frustration — is politically untenable.

In the News

Sydney Metro City & Southwest opens to passengers in late 2025, delivering Australia’s first fully automated driverless metro railway and setting a new operational benchmark for passenger rail capacity and reliability across Australasian networks.

Sources

| Type | Source |

|---|---|

| IBM | IBM Maximo — “Fleet and Rolling Stock Management Solutions” |

| Industry | Australasian Railway Association — “Passenger Rail in Australia: State of the Industry 2024” |

| Government | Transport for NSW — “Sydney Metro: Program Business Case Summary” |

| Government | BITRE — “Urban Rail Patronage Statistics 2024” |

| Operator | MTR Corporation — Annual Report & Sustainability Report |

| Operator | Metro Trains Melbourne — Franchise Performance Data |

| Government | Public Transport Victoria — Network Performance Reports |

| Statistics | Australian Bureau of Statistics — Regional Population Growth Data |

Next: The Heaviest Trains on Earth · You’ve seen iron ore trains in photos — but have you ever noticed they’re pulling loads heavier than an aircraft carrier?